The first week of April is always an important one in the UK; it marks the implementation of many pieces of legislation. April 6th, 2017 was an all-important date and one in particular caused consternation in the recruitment sector …

Specifically, the public sector IR35 reforms could end up costing recruitment agencies vital money because of the way workers will be taxed in accordance with the changes.

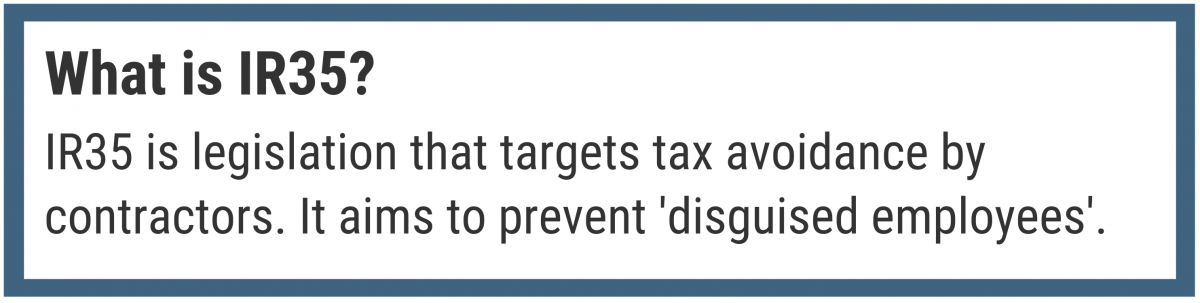

IR35 Explained

Initially introduced by HMRC back in April 2000, the aim of IR35 was to combat abuse by any individual who would be treated as a full-time employee were it not for the fact they provide work via their own personal service companies (PSCs).

The changes have been made to close a loophole which allows people working full time to be seen as freelance, therefore changing the way they are taxed.

Under the reforms, IR35 status has to be determined by a client, rather than contractor, who will then have their tax and National Insurance Contributions (NICs) deducted at source via PAYE.

Agencies that cannot cater for genuinely outside IR35 contractors will see their profits drop dramatically.

Responsibility rests with the party that pays the contractor, which could be recruitment agencies in some cases. These agencies will have to liaise with and ask their client to give their opinion on the IR35 status of the contractor.

By client in this case, we mean the company the worker is supplying their services to.

Therefore, the fee payer, which could be the client, an agency or any other third party paying the intermediary, will calculate any tax and NICs, and pay straight to HMRC, with the money coming out of the fee for any work provided.

The worker is then able to set against its own tax and NICs liability for the tax year, an amount equivalent to the payment received from the fee payer that has already had all tax deductions taken from it.

Why are IR35 reforms in place?

The reforms are here, in short, to stop people who look and seem like contractors but are working full time for a company, avoiding having to pay the same tax that somebody would who is contracted by an organisation.

HMRC will closely monitor the relationship between a limited company and agency / public sector body to monitor working practices.

We have seen contractors blackball the public sector over the recent IR35 reforms, and my prediction is that the same will happen when (not if) the IR35 rules are rolled out to the private sector.

Telltale signs include work on a daily basis, and the control exerted by an organisation over the limited company.

Usually, somebody who is self-employed can work for an organisation but not be subject to their control; the contractor will work a number of hours but have control over their own hours.

The change comes if, for example, the employer is able to name a time, place, hours and the task to be undertaken. If the employer has sufficient control to move a contractor from job to job, there’s an element of control here, which indicates employment.

Although not always the defining factor – and it doesn’t have to be administered directly – control is a decent indicator.

In those instances, the employer will be required to calculate income tax and NICs, as per the requirements IR35 reforms.

A worker / client / PSC, for their part, are responsible for giving the public sector client / agency all the information needed to determine whether off-payroll rules apply.

The agencies supplying the public will see an increased administration burden but that is an ongoing trend.

Indeed, where they do apply, the worker should provide any information needed to deduct tax and NICs from the payment they make to the intermediary.

How recruiters feel about the IR35 reforms

Recruiters were naturally concerned over the possibility that they would be liable for any tax shortfalls from the contractors that they source for clients.

However, the government have recently released a Finance Bill which goes some way to cooling these worries.

Under this, it confirms the ‘client’ or ‘hirer’ are the ones responsible for any tax shortfalls, as well as deciding if the contractor falls inside IR35.

Despite these reassurances, it doesn’t mean recruitment agencies won’t feel any effects from the IR35 reforms.

One of the recruitment agencies we spoke to commented on how they are pleased that a loophole is being closed.

The arrival of the legislation has been much heralded and its impact much maligned as a move that will undoubtedly impose a significant burden on an already over stretched public sector and puts agencies in the frame, making them responsible for carrying out HMRC’s enforcement work, which is wrong.

These are the thoughts of Cameron Ford at Reflect Recruitment Group Ltd, who provide staff for a variety of different industries.

The business is one of the agencies that treat temporary staff they provide to clients as PAYE temporary workers and pay them directly rather than through third party payroll providers.

Cameron said: “There has long been a loophole which has allowed recruitment agencies to avoid not only employers’ NI and holiday pay but also employees’ NI contributions which has been exploited.

“We are extremely pleased to see the beginning of the closing of that loophole with the changes in the public sector.”

The Association of Professional Staffing Companies (APSCo), said that recruitment agencies are still open to liabilities if a client says it has taken reasonable care when deciding whether an engagement is akin to employment or self-employment.

Samantha Hurley, Head of Operations at APSCo, said: “Recruiters working with public sector organisations must continue to be vigilant and question determinations that they feel are inaccurate.”

However, Samantha feels that the introduction of ‘reasonable care’ ultimately is good news for recruitment agencies.

“Firms working with professionals in the public sector aren’t tax experts. They also have no visibility of how a role is undertaken on the client site, or indeed how the contractor runs his or her PSC or LLP and so are ill-equipped to determine tax status.

“The reasonable care provision, which was dropped into the legislation at the 11th hour, puts the onus back onto the client. This is helpful for our members and we’re glad this was included.”

Changes needed to prevent exploitation

However, Reflect Recruitment don’t feel that enough has been done. Although one loophole has been closed due to the IR35 changes, the business feel another is opened.

Cameron explained: “There is a further loophole being exploited where agencies are using a third party payroll provider to pay temporary staff on a PAYE payroll but, where in the process of running payroll, they charge the temporary member of staff their own employees’ NI, a payroll charge, but also the employers’ NI that the agency or payroll company should be paying.”

In the absence of proper guidance at an early stage, we are seeing end clients with no option but to issue blanket bans on PSCs.

These third parties are also taking advantage of the NI relief of £3,000 by essentially grouping a small number of workers into different companies so that they themselves can get that relief intended for small employers.

As an organisation that pays fees for its employees, Reflect Recruitment regard both practices as “equally unethical and consistently press for a reform of the ability for recruiters and the huge industry of umbrella and payroll companies to be able to continue to do this.”

What risks could IR35 pose for recruitment agencies?

Contractor Calculator, which is an online portal that provides free expert advice and guidance to freelancers and contractors, believes agencies – and the public sector – will suffer in the long term because of these changes.

The company’s CEO, Dave Chaplin, expects a similar experience to when IR35 was first introduced and as a result, agencies will see a ‘dramatic’ drop in profits.

He said: “I was a contractor in 1999 when the original IR35 was first proposed. The demand for top-end IT contractors then was very high, like it is today, and agencies who could not offer outside IR35 contract arrangements were blackballed by contractors.

“We have seen contractors blackball the public sector over the recent IR35 reforms, and my prediction is that the same will happen when (not if) the IR35 rules are rolled out to the private sector.

“Agencies that cannot cater for genuinely outside IR35 contractors will see their profits drop dramatically.”

Under the reforms, IR35 status has to be determined by a client, rather than contractor, who will then have their tax and National Insurance Contributions (NICs) deducted at source via PAYE.

Global resourcing experts, BPS World, believe that the changes will have both positive and negative consequences.

Kris Simpson, the company’s Compliance Manager, believes that it will push limited company contractors towards the private sector, leaving the public sector with a challenge to hold onto these workers without incurring an increase in cost.

He explained how he feels agencies will be affected.

“The agencies supplying the public will see an increased administration burden but that is an ongoing trend that all agencies have had to get resilient to due to a series of legislation changes over the past few years.”

What should agencies be mindful of?

We’re already seeing the impact of the IR35 reforms according to Julia Kermode, Chief Executive at the Freelancer & Contractor Services Association (FCSA).

Julia feels the changes are unfair to agencies.

“The arrival of the legislation has been much heralded and its impact much maligned as a move that will undoubtedly impose a significant burden on an already over stretched public sector and puts agencies in the frame, making them responsible for carrying out HMRC’s enforcement work, which is wrong.”

If the employer has sufficient control to move a contractor from job to job, there’s an element of control here, which indicates employment.

The fear is that recruiters will push agencies towards umbrella firms who will calculate any impact of deductions including employers’ NICs, assignment rate and resulting gross pay for contractors.

However, Julia warned: “I want to fire a note of caution to agencies and contractors when choosing umbrella firms to partner with – there are a lot of newcomers entering the market with no track record so due diligence is essential to minimise risk for all parties.”

Wider consequences of IR35 reforms

Of course, with any legislation of this magnitude, there are effects that stretch much further than recruitment agencies – some of which already observed by Julia Kermode.

She cited incidences of locum doctors failing to turn up for shifts and IT contractors abandoning public sector projects.

The FCSA believe that, contrary to government assertion that only those not compliant with IR35 legislation will be affected, this isn’t the case in practice.

Julia said: “In the absence of proper guidance at an early stage, we are seeing end clients with no option but to issue blanket bans on PSCs or make wholesale decisions that all contractors are caught by IR35, with significant consequences for the supply chain.”

There has long been a loophole which has allowed recruitment agencies to avoid not only employers’ NI and holiday pay but also employees’ NI contributions which has been exploited.

We’re only a month into the reforms so it’s hard to know just how agencies will be affected in the long term.

What is certain though is everybody would have benefited from better guidance in the organic stages of the reforms.

Agencies, for their part, are mixed on the news, some welcoming the closing of loopholes, while hoping for more.

It seems certain though they will see an increase in administration and there is a danger of a drop in profits. Recruiters will therefore have to tread carefully when planning their next steps, while ensuring their actions satisfy the reforms.

What is your recruitment agency planning to do about the changes? We’d be very interested to hear about your experiences.